It’s 2025. So why does our industry sometimes seem to be stuck in the 1990s? The time has come for a 21st century pension service.

We have a Labour government with a landslide majority, Oasis are getting ready to tour, Peter Mandelson is back, and hedonism is in fashion again with the young (or so I am told).

Cultural commentators say they detect echoes of the 1990s, though without the booming economy. And when it comes to pensions administration there’s that feeling too – but not in a good way.

Our world is shaped by fast-moving technology, demographic shifts, evolving consumer expectations, and tighter budgets. Yet as other parts of the financial sector adapt, inside our pensions industry bubble many things are little changed since the leaders of New Labour linked arms to welcome in the new millennium.

Compare pension schemes with retail banks

Look at retail banking, where innovative startups are recruiting Millennial and Gen Z customers. This is prompting the high street lenders to respond with improved digital features such as help with budgeting, temporary card freezes and instant notifications – all supplied through ever-evolving apps.

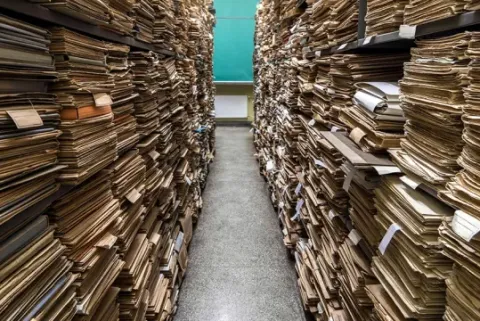

Now look at pension schemes. Despite repeated entreaties from bodies such as the Pensions Administration Standards Association, many schemes still have member data stored in paper files or on microfiche. And we continue to send out complex, cumbersome paper forms that can cause stress for older members or dependants dealing with bereavement.

We aren’t keeping pace with the digital transformation in the wider financial services industry. Halfway through the 2020s, it’s time we shaped up. The Pensions Regulator (TPR) made this clear in its recent data strategy, which is a wake-up call for action.

In this article, I’ll set out what we mean by a 21st century pension service and look at some of the forces driving change in what we at Aptia call the Administration Age. I’ve adapted the themes from our white paper about the importance of good data – and good data is vital if your pension scheme is going to rise to the challenge.

Pensions dashboards will kickstart change

Change will be kickstarted next month when the first batch of large pension schemes connect to the pensions dashboards ecosystem. When dashboards go live, 16 million savers will be able to see all their pensions in one place for the first time.

Pensions dashboards will help drive improvement, but there is much more we must do to deliver a pension service fit for today.

Here are some key, often interlinked features:

- Complying with laws and rules: UK pension schemes are governed by an ever-growing array of laws and rules. In addition to pensions dashboards, pension schemes face new governance requirements and must abide by the principles of regulations such as the Financial Conduct Authority’s value for money regime and consumer duty. With the government carrying out a market review of the pensions industry, we don’t expect any let-up in the regulatory workload soon

- Adapting to demographic change: as the UK population ages and baby boomers retire, the role of pension schemes is shifting from helping people save for retirement towards supporting them and their beneficiaries as they manage their pension pots. But we also have to prepare for the next wave of pension savers, such as Gen Z, who will have new challenges. We must provide better, simpler services that make life easier for people

- Responding to technological advances: the age of digital pensions administration will be based on business process automation, robotics and artificial intelligence. These innovations will make us more efficient, leaving human administrators to deal with more complex problems. At Aptia, we are about to launch our first app for pension scheme members, and we are working on digital forms that make form-filling less stressful

- Meeting rising expectations: consumer expectations have been driven higher by the ease and information provided by the internet and digital devices. People want to manage their lives with a click on their phone or tablet – and that includes pension scheme members. And regulation is driving up standards for how financial firms treat consumers – especially vulnerable customers

- Consolidating and simplifying: with many DB schemes in surplus, pension scheme consolidation is high on the agenda. The total for bulk annuity purchases is predicted to be about £50 billion this year as trustees seek to secure their members’ benefits. And, especially when Guaranteed Minimum Pension equalisation (GMPE) is completed, there is plenty of scope to simplify benefit structures

- Navigating the capacity crunch: these trends are happening against a backdrop of dwindling capacity for pensions expertise as administrators with valuable knowledge of scheme histories leave or retire. And as projects stack up, the workload for pension schemes is increasing even as the pool of DB administration skills shrinks

Good data is vital to meet these challenges

As we argue in our white paper, good data is fundamental to delivering the pension service that will result from these aims and pressures.

For example:

- Without clean, correct data, no pension scheme will be ready to connect to the dashboards ecosystem. And TPR’s demand for high-quality, accessible data recognises the importance of properly maintained information to comply with its rules

- We can utilise data to generate analytics that help us understand our members and provide them with the features they need. And we can simplify our processes to make it easier for older, potentially vulnerable people to use our services

- To become more efficient and emulate innovations elsewhere, we need to digitise our data and keep it accurate. Pensions dashboards will evolve and are likely to become part of the open finance revolution – covering other forms of saving, offering guidance and eventually transactional capabilities

- Without good data, we won’t be able to meet rising expectations – whether those of consumers in the digital age or regulators pressing us to provide better value and customer care. TPR made this point in its recent data strategy

- If, like many DB schemes, you are targeting buyout or another derisking strategy, or are contemplating run-on, you must have good data. Too many transactions are held up or made more costly by poorly maintained information – and that includes GMP rectification, reconciliation and equalisation

- Our industry’s capacity crunch is intensifying, and in the long run we will rely more on automation to keep records up to date and make benefit calculations. To automate, you need good data

A pension service for the Administration Age

We have written before about the Administration Age – our name for the new era that puts pensions administration at the heart of pensions delivery. If the Administration Age is the backdrop to change, then the 21st century pension service is the long-overdue result.

So don’t look back (in anger or otherwise). The 21st century pension service brings together good data, technology, streamlined processes and our industry’s best thinking and instincts to meet the requirements of pension schemes and members today.

You can read our white paper – Good Data: Why It Matters, How to Get It, How to Keep It – by clicking here.